Intuit Quickbooks Point of Sale Basic V11 2016 New User

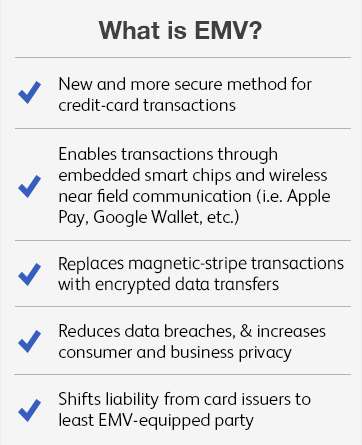

EMV is a new standard for credit-card payments that is meant to make credit transactions more secure throughout the globe.

EMV has already been implemented in most developed countries around the world. As one of the final major markets to make the move, businesses across the U.S. are now scrambling to initiate and finalize the transition before the October 1, 2015, deadline, which denotes a major shift in liability.

For a better understanding on how it works and how it benefits your business and its customers, read through this guide. To jump right in to the actual process, check out our step-by-step guide to EMV migration.

Is “EMV” Synonymous With “Smart Chip?”

No.

While it’s tempting to make these terms interchangeable, the truth is that they are not. EMV payments can be made using an embedded chip or wirelessly through terminals that support “contactless” EMV payments.

For accuracy, it’s best to call the chip itself an “EMV chip.”

Okay, So What’s the Deal With EMV Chips?

Okay, So What’s the Deal With EMV Chips?

In one word, security.

EMV chips have been used to substantially reduce counterfeit credit-card fraud in major markets over the past decade.

For example, the United Kingdom has been very successful at reducing credit-card fraud since its own EMV migration. Since introducing EMV-chipped cards into its market, face-to-face credit-card fraud has dropped a whopping 72%. A similar trend took place in Canada, where, between 2011 and 2016 (the years immediately following Canada’s migration to EMV-chipped cards), domestic counterfeit fraud dropped 42%.

So as EMV chips went into markets, counterfeiters made their way into unprotected markets, mainly the U.S. In 2016, global credit-card fraud totaled $14 billion, of which the U.S.’ portion was 51%. U.S. credit-card fraud also increased at a higher rate than the rest of the globe (29% compared with 11%, respectfully).